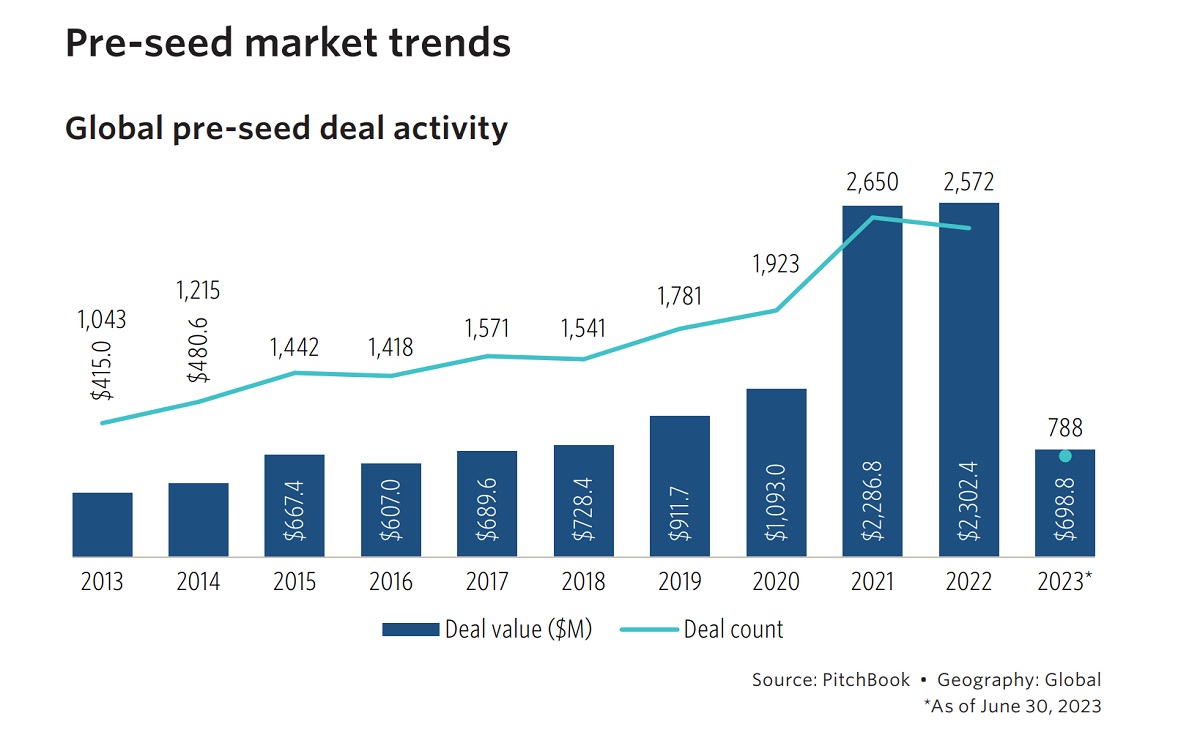

Global VC deals declined in Q3 for the second quarter in a row, hitting 3-year lows

[ad_1]

Global venture capital deals declined in the third quarter for the second consecutive quarter, falling to the lowest level since the second quarter of 2020.

Deal value fell to $73 billion, which is lower than the record by more than 65%, according to the latest first look at a report from PitchBook and the National Venture Capital Association (NVCA) upcoming Q3 2023 Venture Monitor.

As regions go, Asia showed the lowest decline, with quarterly deal counts falling just 10% from the quarter before. Europe and Latin America, on the other hand, saw declines of more than 30% based on preliminary data. Europe did, however, show growth in total invested capital, said PitchBook VC analysts Kyle Stanford and Nalin Patel.

They said that exits aren’t climbing back yet on a global basis compared to the recent past. While total exit value did grow from the three prior quarters, it remains well below the highs of a couple years ago and continues to pressure the global dealmaking environment.

Event

GamesBeat Next 2023

Join the GamesBeat community in San Francisco this October 24-25. You’ll hear from the brightest minds within the gaming industry on latest developments and their take on the future of gaming.

Learn More

On an annual basis, all global regions are lagging in the fundraising department except for Latin America, which has raised the same amount as 2022. However, fundraising within Latin America is much lower than other regions due to its nascency as a venture market.

“We expect the low fundraising totals from this year to have impact on VC activity in 2024, even as many investors point to next year as a rebound year for the market,” the analysts said.

U.S. stalled

After several quarters of slow growth in the number of deals completed, the market continued to show a decline in total deal count during Q3, Stanford said.

The most significant declines came at the later stages of VC where the poor exit market has continued to pressure dealmaking. Deal sizes and valuations through the first three quarters of 2023 have also showed significant declines from last year, especially at the late-stage and venture growth-stage.

The median venture growth stage deal size is at its lowest annual point since 2016, while valuations for the stage have fallen to 2018 levels. The continued slow exit market is causing increasing pressure on the stage which sits closest to the exit markets.

The pullback from large institutional investors that have been vital to supporting companies late in their venture lifecycle has made it increasingly difficult for deals to get done, let alone the large-sized deals that many companies need.

The Q3 exit landscape showed little sign of improvement after a languid preceding 18 months, particularly as several high-profile IPOs failed to induce optimism for the rest of the year.

During Q3, there were nearly 300 exit events totaling $35.8 billion in cumulative exit value, marking the most substantial performance since Q4 2021. However, this seemingly positive trend is tempered by the fact that over half of this exit value came from just two IPOs: Klaviyo and Instacart.

Despite being profitable, these companies experienced notable valuation cuts compared to their previous private funding rounds, raising concerns about the challenges facing unprofitable or growth-focused tech unicorns in the public markets.

Beyond IPOs, acquisition deal value increased from Q2 but remained historically low, while quarterly deal count in Q3 came in at its lowest in over a decade.

In all, the Q3 exit environment was a mixed bag, showing some promise with profitable IPOs but also highlighting the dilemma companies face between going public with potentially reduced valuations or staying in the uncertain private markets, Stanford said.

Fundraising showed little change during Q3. For the year-to-date, just $42.7 billion has been raised, setting 2023 on pace to reach the lowest full-year total since 2017. Slow fundraising is in large part due to exit markets returning little in the way of gains back to VCs and LPs, Stanford said.

“With high hopes for a rebound in 2024, the market is certainly hoping that Q4 can show signs of growth,” Stanford said. “Though low fundraising numbers from this year don’t bode well for future dealmaking growth, the records amount of US fundraising in 2021 and 2022 can bolster cash reserves for the near term.”

Europe decelerated

Through Q3 2023, European VC deal activity decelerated from 2022 levels, said Patel. Despite the drop off in quarterly figures from 2022, deal value remained flat in Q3 and Q2 2023.

Dealmaking has slowed in line with market expectations as a tougher growth and funding landscape for startups has persisted. Counts were also down quarter over quarter, further indication that fewer deals are getting over the line as GPs become more prudent with their capital deployment.

Exit activity through Q3 2023 is down from the pace set throughout 2022. However, exit value generated in Q3 2023 was slightly up from Q2. Substantial exits have been scarce through Q3 2023, with founders and investors unwilling to risk an exit amid choppy public markets.

There are reports of notable VC-backed companies targeting an exit; however, PitchBook expect exits to remain subdued until greater valuation and macroeconomic clarity is established, Patel said.

Capital raised by European VC funds has continued to accumulate in 2023. Fundraising through Q3 2023 is tracing below the annual run rate for 2022.

The factors include inflation, high interest rates, and weak growth. These problems have impacted sentiment across financial markets. As a result, fundraising conditions have become more challenging considering the record amounts raised in recent years, Patel said.

GamesBeat’s creed when covering the game industry is “where passion meets business.” What does this mean? We want to tell you how the news matters to you — not just as a decision-maker at a game studio, but also as a fan of games. Whether you read our articles, listen to our podcasts, or watch our videos, GamesBeat will help you learn about the industry and enjoy engaging with it. Discover our Briefings.

[ad_2]

Source link